The global microchip shortage has become headline news, as repercussions

have spread from core technology products to other chip-heavy consumer

goods — from autos to appliances and beyond. But while the unique

circumstances of the pandemic brought the supply/demand dynamics of

the chip industry to the brink, it can be argued that the path to the crisis

started decades ago. And as the pandemic hit, an unlikely but powerful

set of factors combined to create an unprecedented shortage of one of

the basic building blocks of our increasingly digital society.

Columbia Threadneedle analysts and investment leaders with a long history

of researching and investing in technology came together to discuss the

story behind the semiconductor shortage, how it happened and what we

can expect next.

Question: It’s been said that the chip shortage was along time coming. What were some of the trends in

supply and demand leading up to the current situation?

Paul Wick: The dynamics we’re seeing play out today have been building for a while. Digital semiconductor companies used to have their own production

facilities. In the 1990s that started to change as the industry increasingly

moved to outsourcing manufacturing to fabricators in Asia, mostly in Taiwan.

So, instead of 40 large chip companies with their own facilities running at

70% or 80% utilization, you have a handful of dedicated fabricators that tend

to run their factories at 90% plus utilization, which is much more effi cient. As

a consequence, there’s a lot less slack in semiconductor capacity.

Sanjay Devgan: The way semiconductor companies hold inventory has also

changed. Before the tech bubble in 2000, most original equipment

manufacturers (OEMs) carried chip inventory on their balance sheets. One

of the most infamous inventory write-downs in history was a $2.7 billion

write-down by one of the big OEMs when the bubble burst. They no longer

wanted to take that risk. So, over the last 20 years inventory on the balance sheets — and in the warehouses — of the OEMs has come down and the

inventory on the balance sheets of semi suppliers has gone up.

David Egan: Concurrently, we’ve been witnessing a dramatic growth in tech intensity. Personal

computers in the 1990s. Phones and then smartphones in the 2000s. And the soon-to-be

gigantic companies that were building businesses around mobile internet — the Amazons and

the Googles. At the same time, businesses in many industries were undergoing digital

transformations. All of this added up to a steady increase in demand for semiconductors.

Question: How did the COVID-19 pandemic impact the current shortage?

Rahul Narang: There was a basic miscalculation of how COVID-19 was going to impact the world

economies. Most assumed companies would cut back production as times were getting diffi cult, but demand proved to be quite resilient — even growing for some categories. People were stuck

at home and buying and using more technology, whether it was new or additional PCs, bigger

displays, 4K TVs, game consoles, remote meetings, etc. A sort of perfect storm formed that

combined the demand miscalculation with lean inventories and a surprising consumer appetite

for products full of microchips.

Charles Mann: Automakers in particular were hard hit, as they were unable to reinstate canceled

chip orders when they realized consumers looking for safe transportation in the pandemic

wanted more cars, not fewer. As cars have gotten more complex, data-driven and automated, the

auto industry has become one of the major consumers of microchips. Chips have begun to take

on and evolve into a new role in the automotive supply chain, becoming central to it – not only

because of the “smart” content, but also the data sharing capabilities. In some cases, they’ve

become so central that the lack of one specific, unremarkable chip can bring production to a

virtual standstill.

David Egan: On the supply side, COVID restrictions on factory workers and international trade

slowed production and delivery. On top of the pandemic disruptions, there was a fire in a major

substrate facility (a key part of the chip packaging) in Asia. This affects things like gaming

processors and networking equipment. We’ve seen reports that this has pushed product back

from some companies for more than a year. And in February, the polar vortex in Texas shut down

a number of big facilities, creating even more chinks in the semiconductor supply chain.

David Egan: On the supply side, COVID restrictions on factory workers and international trade

slowed production and delivery. On top of the pandemic disruptions, there was a fire in a major

substrate facility (a key part of the chip packaging) in Asia. This affects things like gaming

processors and networking equipment. We’ve seen reports that this has pushed product back

from some companies for more than a year. And in February, the polar vortex in Texas shut down

a number of big facilities, creating even more chinks in the semiconductor supply chain.

Question: How will this situation be resolved? What is the path

forward for the industry in the next couple of years?

Rahul Narang: It’s important to remember that some powerful longer term trends were also a factor in the resilience of demand during this crisis. The move to 5G, digital payments, digital

enterprise transformation, cloud computing, cybersecurity, AI, autonomous driving, electric

vehicles, battery technology and more. These are all things we’re watching closely, and when we

step back and look at these themes, we feel that this pandemic has kind of hit what I’d call a

giant fast forward button to the future for many of them.

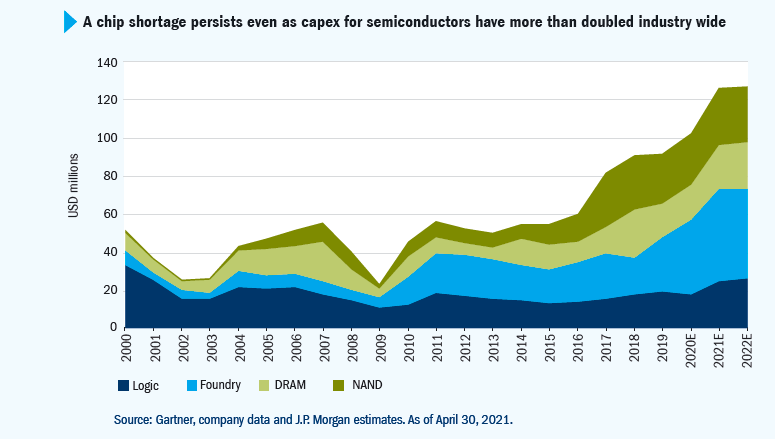

Sanjay Devgan: From an investment standpoint, visibility for the semiconductor industry is probably at an all time high. Historically with semis, when you place an order, the order is only

good for that quarter. And then you have to build the backlog for the next quarter. One major firm

is leading a change in that paradigm, offering what they call a “preferred supplier program.” If you

give them one year’s worth of non-cancelable orders, then they will move you to the front of the

supply queue. Basically, this gives the company revenue visibility out for a year. And we’re seeing

this type of thing happening across the entire industry. We’re also seeing that pricing from the

foundries is going up, as well as materials prices, and the semi companies are able to pass that

onto their customers on a cost-plus basis.

Sanjay Devgan: From an investment standpoint, visibility for the semiconductor industry is probably at an all time high. Historically with semis, when you place an order, the order is only

good for that quarter. And then you have to build the backlog for the next quarter. One major firm

is leading a change in that paradigm, offering what they call a “preferred supplier program.” If you

give them one year’s worth of non-cancelable orders, then they will move you to the front of the

supply queue. Basically, this gives the company revenue visibility out for a year. And we’re seeing

this type of thing happening across the entire industry. We’re also seeing that pricing from the

foundries is going up, as well as materials prices, and the semi companies are able to pass that

onto their customers on a cost-plus basis.

The bottom line is that from the current vantage point, industry analysts and

semiconductor companies are predicting chip shortages until the end of the year, and

in some situations, into 2022. Despite this setback, we see the key demand drivers for

technology continuing relatively unabated — some even accelerated by the realities and

lessons of the pandemic.

As the pandemic economy fades, we expect to see a slow, and hopefully orderly, shakeout of the chip shortage over the next 9-to-12 months. Over that time, our team

sees strong fundamentals, and opportunities for value in the semiconductor sector, including equipment suppliers, OEMS and manufacturers, against continued broad and

strong demand. Compelling growth trends in advancing and emerging technologies also

have the potential to provide support for expanded capacity and chip supply over the

longer term.