In 2022 we expect the market narrative to transition to the traditional expansionary phase of the business cycle. Here’s what it means for fixed income investors.

Monetary headwinds

Throughout 2021 the invisible hand of easy global monetary

policy supported financial markets. For 2022, however, the

outlook is quite different. We have already seen central banks

pare asset purchases, and we should expect a very different

backdrop for short-term interest rates, pricing in rate hikes

for most major central banks. This waning monetary support,

coupled with expensive starting valuations, warrants a more

selective approach to fixed income in 2022.

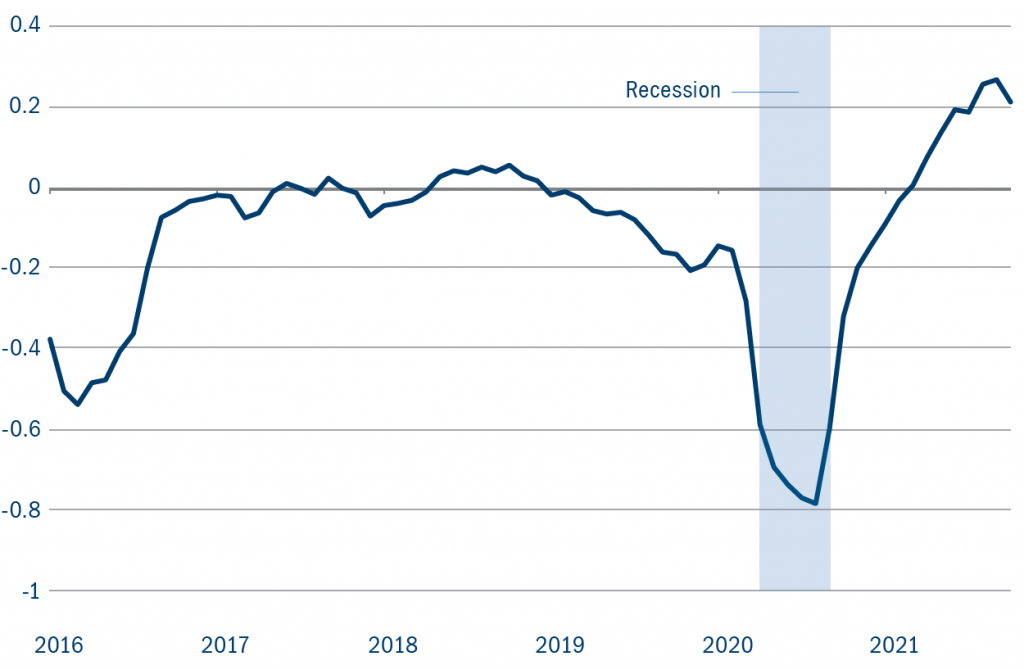

Star potential

During recessions it is common for rating agencies to

downgrade companies whose economic fortunes begin

to dim. The volume of these “fallen angels” during the

pandemic was historic – $184 billion of corporate debt lost

its investment grade (IG) status.1 Aggressive management

of costs, capital expenditures, dividends, share buybacks

and capital structures all helped stabilise corporate cash

balances. As demand steadily returned, profit margins and

free cash flow grew rapidly allowing companies to pay down

debt and improve credit quality. We believe 2022 will be a

strong year for “rising stars” as many high yield companies

achieve IG status (Figure 1). In an environment where price appreciation appears muted, rising star candidates could represent a

rare opportunity for gains. Risk premiums between BB- and BBB-rated

bonds still offer value and prices could rise as investors anticipate higher

ratings. But it takes targeted fundamental credit research to identify these

favorable credit stories ahead of ratings agency action.

Figure 1: Rising stars: credit upgrades for high yield companies are

outpacing post-recession downgrades

Source: Bank of America/Macrobond, October 2021. High yield credit migration rates: trailing six-month net upgrades as a

percentage of market value, 1 January 2016 – 31 October 2021

Off-benchmark benefits

The Covid-induced liquidity wave pushed investors back into financial markets

globally and drove valuations to historically expensive levels across most

liquid bond markets. The notable exceptions are bonds that are less liquid,

less followed or less benchmarked. This is particularly true in structured

credit and municipal bonds. Nearly 40% of mortgage- and asset-backed

securities are not included in any benchmark, including most of the higher

yielding opportunities in that universe. The same dynamic occurs in the

municipal bond space, where a high degree of fragmentation, small issue

sizes and frequent absence of credit ratings mean that muni benchmarks

don’t include a lot of the opportunity set. In each case, a research-driven

active strategy can flesh out the risk-reward trade-off in these areas to

generate higher income and return prospects than passive alternatives.

From recovery to expansion

In 2022 we expect the market narrative to transition from the “shock

and awe” of the pandemic to the traditional expansionary phase of the

business cycle. In this stage bond investors benefit far less from owning

generic market risk as central banks move toward the exits. A much more

targeted approach, focused on improving corporate and consumer balance

sheets, should lead to better outcomes in 2022.

Macro/Government Bonds 2021-22

By Adrian Hilton, Head of Global Rates and Currency

2021 will be remembered as a year in which the word “transitory” was

used more often than normal. Specific to the market it relates to the battle

between rising inflation expectations and the idea that present outsized

levels of price rises will rebalance in the coming year, once transitory

factors such as the reopening of the economy, supply chain shortages

(both labour and capital) and surging energy increases are behind us.

It was, as a result, a hard year for core government bonds. Yields

and inflation expectations rose through much the year and returns

were negative. All the while, central bank rhetoric erred on the side of

dovishness – but frequently failed to win market confidence or support.

Our own view of lower for longer growth, inflation and bond yields was

challenged, making it a more difficult year for our funds at times.

What of the outlook? We feel this extraordinary type of inflationary

pressure is unlikely to be repeatable and will not be met with sustainable

pay rises. Thus, negative real wage growth, fiscal headwinds – particularly

in the UK – and tighter monetary policy at the margin will weigh on

economies after the strong rebound of this year.

Government bond markets should take comfort from this – and so an

outcome of better returns in 2022 than 2021 is our central forecast.

Investment Grade 2021-22

By Alasdair Ross, Head of Investment Grade Credit, EMEA

For investment grade credit markets, 2021 will be best remembered as a

year of low spread volatility – which was in stark contrast to the preceding

12 months. Global IG spreads traded in a range of around 20bps from

January 2021 to mid-November 2021, while 2020 saw a much wider range

in excess of 240bps.

This very low level of volatility and dispersion creates a more difficult

environment for active management, and while most of our funds have

outperformed this year, the extent of that outperformance is lower than

last year.

What of the outlook for the coming year? We feel fairly neutral about the

level of spreads. This reflects the balance between positive fundamentals

and expensive valuations. Specifically, while policy conditions appear to

be moving slowly in the “wrong direction”, the present low and/or negative

rates of interest and assumed future levels will continue to provide a

positive backdrop for the market.

Secondly, the global economy may be slowing a little – but for IG credit a “not

too hot, not too cold” low but positive growth environment is ideal. It creates

an atmosphere that helps rein in excessive animal spirits in the boardroom

yet doesn’t produce a risk of significant downgrades or worse. Corporate

credit quality is also heading in the right direction and we expect key metrics

to revisit where they were at the end of 2019 by the end of this year.

Lastly, we still expect to see demand for income-generating asset classes

with lower risk such as IG credit – this at a time of lower new issuance and

ongoing central bank buying in Europe.

So why are we not more bullish? The trouble is valuations or spreads.

The present level of credit spread is well through both shorter term (fiveyear)

and longer term (20-year) averages and a little over 0.5 standard

deviations expensive to the latter.

High yield 2021-22

By Roman Gaiser, Head of High Yield, EMEA

For European high yield credit markets, 2021 will be remembered as the

year of improving credit quality seen through both the return of rising stars

as well as the fall of default expectations to sub 1% levels. This was in

sharp contrast to 2020 where the market size and credit quality grew due

to the number and type of issuers who joined the EHY universe as falling

angels and default expectations almost reached double-digit levels.

EHY spreads have done a 100bps round trip in the past 12 months with

the lows reached in mid-September. Credit spreads fell back to pre-Covid

levels, helped by improving corporate fundamentals and positive credit

rating progress. This led to lower default expectations as central banks

continued to stick with lower for longer – providing good support for the

asset class.

What of the coming year? The EHY outlook continues to be supported by

a positive growth outlook and improved corporate fundamentals. Rising

numbers of Covid cases, as well as recent developments around the

Omicron variant, are a reminder of the risk. But efforts to avoid lockdowns

to support an improving economic picture remain a key aim of most

governments. Market technicals appear balanced: inflation worries linked to supply and labour shortages, as well as logistics disruptions, put

pressure on government yield curves, and central banks appear to move

away from loose monetary policy.

But appetite for income and higher yielding assets remains good and new

issuers coming to markets offer opportunities. With spreads now almost

100bps higher than the 2021 lows and back to the levels seen 12 months

ago, valuations look fair despite recent increased uncertainty. Expectations

of an ongoing post-pandemic economic recovery appear priced in, while

default concerns have fallen to historical lows. With risk premia near

historically low levels, there is some concern that compensation for

unanticipated volatility is limited. Still, with a yield pick-up and moderate

duration, the EHY market offers opportunities.